Key points about ACA reporting:

- The Affordable Care Act (ACA) requires some employers to gather information regarding the healthcare coverage they offer their employees.

- If you’re an Applicable Large Employer (ALE) or offer self-insured plans, you’re required to submit ACA-related reports.

- Our checklist outlines important guidelines, deadlines, and everything else you need to know to prepare for ACA compliance this year

This information has been updated as of February 2023.

As the end of the year approaches, so does Affordable Care Act (ACA) reporting. Regardless of whether or not you’re a fan of this legislation, we’re here to help you stay compliant and prepare for this year’s reporting requirements.

What is the ACA?

The ACA, also referred to as “Obamacare,” was enacted in March 2010. Essentially, the Act aims to give more people access to affordable healthcare.

What is ACA reporting?

The ACA requires applicable employers to gather and submit information regarding the employee healthcare coverage they offered each calendar year. ACA reporting refers to the process of submitting forms to the Internal Revenue Service (IRS) and sharing copies with employees.

What is ACA compliance?

Companies subject to the ACA must provide affordable health insurance that meets the minimum essential coverage and minimum value standards for at least 95% of their full-time employees (as well as their dependents).

To comply with the ACA, companies must also provide their employees with the following:

- Notice of coverage and available benefits.

- A summary of benefits and coverage outlining the offered plans and employee costs.

- Form 1095-C, Employer-Provided Health Insurance Offer and Coverage, that serves as an annual confirmation of offered benefits.

- Form 1095-B, Health Coverage, that serves as an annual confirmation of enrolled benefits (if not an ALE Member and sponsoring a self-insured health plan).

Additionally, Forms 1094-C/1095-C must be submitted to the IRS and all applicable state agencies each tax year to confirm that required businesses offered ACA-compliant coverage to eligible full-time employees each month. Companies must ensure that the data submitted and their business practices match up so that these forms wholly and accurately reflect ACA compliance. Otherwise, the IRS and state agencies may issue penalty notices.

Who has to comply with ACA?

Applicable Large Employers (ALE) are required to file under the ACA. These employers have 50 or more full-time or full-time equivalent (FTE) employees. Please note that this is a general rule – there may be cases in which businesses with less than 50 full-time or FTE employees still need to file.

Employers who offer self-funded or self-insured healthcare must also complete ACA reporting, regardless of their organization’s size.

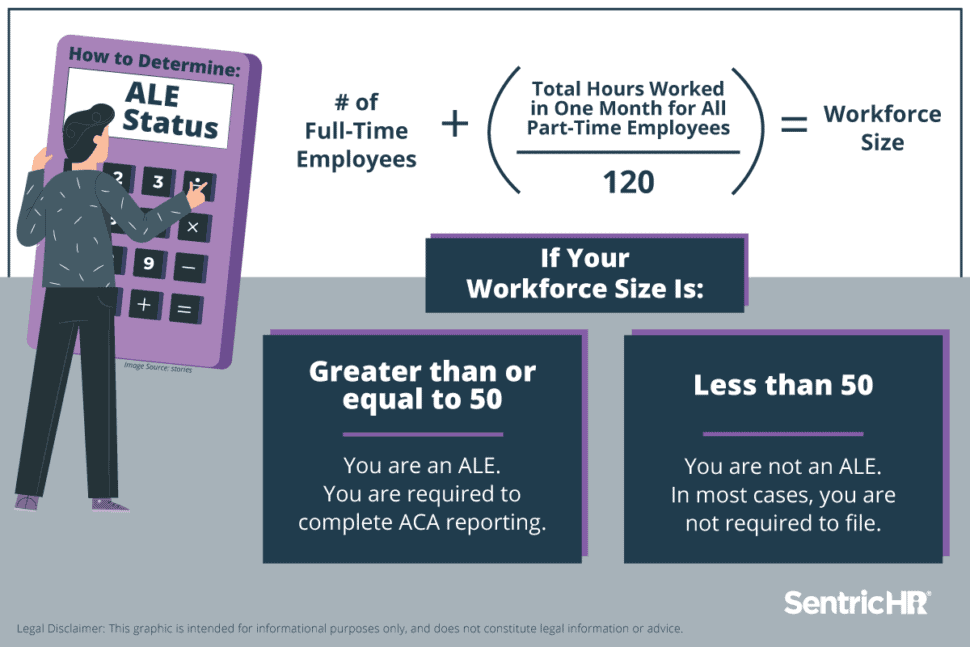

How do I know if I’m an ALE?

To determine your ALE status, you’ll need to perform a few simple calculations. Follow the steps below:

- First, count your number of full-time employees. These are the employees who work at least 30 hours per week (or 130 hours per month) on average.

- Next, count your number of full-time equivalent (FTE) employees. These employees work part-time. When their hours are combined, they’re equivalent to a full-time employee. To determine the number of FTE employees you have, add together all of the hours that part-time employees work in a month. Do not include more than 120 hours per employee.

- Then, divide your total by 120. The result is the number of FTE employees you have.

- Add the number of full-time employees to the number of FTE employees to get your workforce size (if you end with a fraction, round down).

- If this number is greater than or equal to 50, you are an ALE and thus required to complete ACA reporting.

- If this number is less than 50, you are not an ALE. In most cases, you are not required to file.

Here’s a quick example:

Let’s say you have 60 employees. 45 of them work more than 30 hours per week (or 120 hours per month). As a result, you have 45 full-time employees.

The remaining 15 employees work part-time. They each work 60 hours per month. When you add the total hours they work in a month together, you get 900.

15 part-time employees * 60 hours worked per employee for one month = 900 hours

Next, divide your result by 120. You get 7.5, which is the number of FTE employees you have.

900 hours worked / 120 = 7.5 FTE employees

Add the number of full-time employees to the number of FTEs.

45 full-time employees + 7.5 FTE employees = 52.5 full-time, including FTE, employees

Rounding down, your end result is 52. Because this number is greater than 50, you are an ALE and must submit ACA reporting.

All else remaining the same, if you had 40 full-time employees, you would not have been an ALE. Even though you have 60 employees, your workforce count would come out to 47, which is lower than 50.

If you experienced turnover and fell below 50 full-time or FTE employees, you typically do not need to file. The bottom line? Check your ALE status regardless of whether you were an ALE last year or not. Please visit the IRS’s page for more example calculations and additional information.

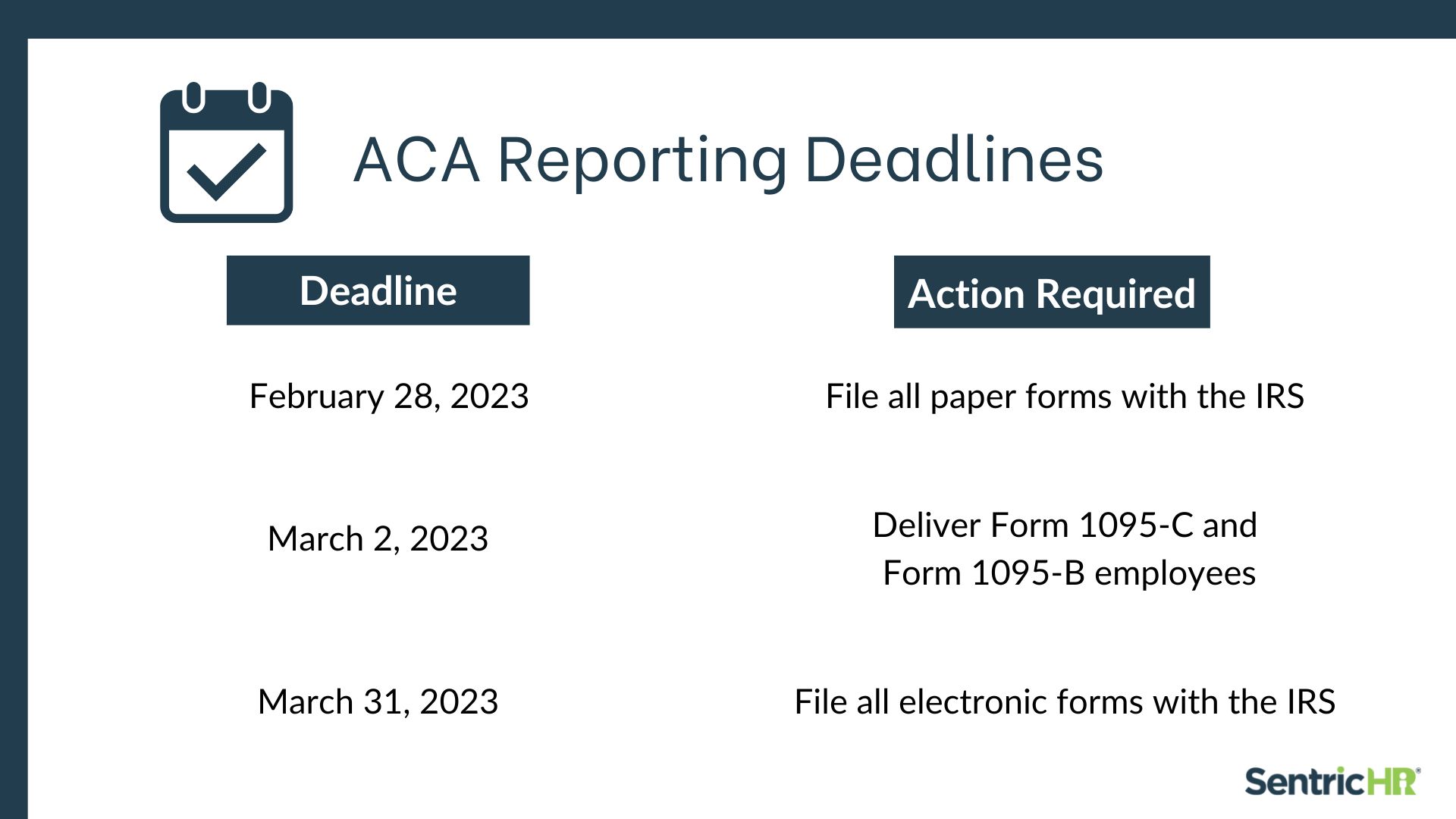

What are the deadlines for ACA reporting?

If you are an ALE, there are 3 main deadlines for ACA reporting:

If you’re an ALE and you file more than 250 Form 1095-C and Form 1094-Cs, you must submit the forms electronically through the ACA Information Returns program.

Are you prepared for ACA reporting?

Our ACA Reporting Prep Checklist helps you keep track of deadlines and everything else you need to prepare for ACA reporting this year.

What are the differences between the ACA Forms?

There are several ACA-related forms and the differences between them can get confusing.

- Form 1095-C provides information about the healthcare coverage the employer offered to employees during the year. Among other information, it includes the coverage and lowest premiums offered. Applicable employers must send this form to every employee eligible for coverage (not just the ones who participated in the plan). They must also send it to the IRS.

- Form 1094-C acts as a “cover sheet” for the Form 1095-C. It includes the employer’s contact information, number of employees, and number of Form 1095-Cs. Applicable employers must send this form to the IRS. They do not need to send it to their employees.

- Form 1095-B provides proof of minimum essential healthcare coverage. Essentially, it shows that the plans the employer offered were ACA-compliant. It contains information such as the coverage provider and effective dates. Applicable employers must send this form to their employees and the IRS. In most cases, the employer’s healthcare provider handles this form on their behalf.

- Form 1094-B acts as a “cover sheet” for the Form 1095-B. It includes information such as the employer’s name and contact information. Applicable employers must send this form to the IRS. They do not need to send it to their employees. In most cases, the employer’s healthcare provider handles this form on their behalf.

What forms do I need to complete?

The forms you need to provide depend on your organization’s size and the type of plan you offer:

If you’re an ALE and offer a fully-insured plan, you must provide the Form 1095-C to your employees and to the IRS. You must also send the Form 1094-C to the IRS. In most cases, your insurance carrier will file Form 1095-B and Form 1094-B for you. Note: If you’re an ALE, you must provide paper copies of the Form 1095-C to your employees, unless they consent to receiving electronic copies.

If you’re an ALE and offer a self-insured plan, you must provide the Form 1095-C to your employees and to the IRS. You must also send the Form 1094-C to the IRS. You do not need to provide the Form 1095-B or Form 1094-B.

If you are not an ALE, but offer a self-insured plan, you must provide Form 1095-B and Form 1094-B. You do not need to provide Form 1095-C or Form 1094-C.

How do I prepare for ACA reporting?

If you start to prepare for these upcoming forms and deadlines now, you can make the process easier for your future self.

Start by reviewing your employee benefits. Affordable benefits are the key to the ACA, so you should be able to answer the following questions:

- Does your plan provide minimum essential coverage and minimum value?

- Is it considered affordable?

Next, verify and update these six pieces of information for each employee:

- Eligibility – Under the ACA, ALEs only need to offer benefits to full-time employees

- Hire Date – Look to see if the employee’s hire (or re-hire) date affects their benefits eligibility

- Termination Date – Confirm that you’ve added the accurate termination dates for all terminated employees, otherwise it may look as though they weren’t offered coverage

- Birth Date – In Part II of the updated Form 1095-C, a new field asks for “Employee’s Age on January 1.” Make sure you know your employees’ birth dates so you can accurately complete this field.

- ACA Status – Note whether the employee is full-time or part-time

- Benefit Enrollment Date – This should be the date your employee enrolled in benefits, not the date of their first benefits deduction in payroll

These preparations can make it much easier to complete your forms later. If you don’t work with ACA compliance software and complete your forms manually, double and triple-check the completed forms.

What else do I need to consider?

In addition to the federal requirements, you must also consider penalties and state mandates.

Penalties

If you’re mandated to report under the ACA and miss a deadline or don’t report at all, you may be subject to various penalties. The IRS may charge you up to $560 per form for inaccurate or missing forms.

State Mandates

There are also individual state mandates that may affect your reporting. For instance, California, Massachusetts, New Jersey, Rhode Island, Vermont, and Washington DC all have their own mandates regarding proof of ACA-equivalent coverage.

The deadlines for state requirements may not be the same as federal IRS deadlines, so be sure to check your local legislation for the most up-to-date information.

How does an HRIS help?

ACA reporting can be difficult and overwhelming, but an HRIS streamlines and simplifies the process. When you use one platform for your HR needs, all of your employee information is in one place. This makes it easier to offer and assign coverage, track dependents, and record the data necessary for ACA reporting.

An HRIS can also reduce human error and catch missing information in your forms. At Sentric, we offer robust ACA compliance and support (including one-on-one reporting assistance) in addition to our all-in-one HR software.

Are you prepared for ACA reporting?

Our ACA Reporting Prep Checklist helps you keep track of deadlines and everything else you need to prepare for ACA reporting this year.