Make Managing Leap Years and Extra Pay Periods Easier!

Download our

Payroll Checklist

Key points:

- Leap years increase the chance of an extra pay period, but this change isn’t exclusive to leap years! The number of pay periods you have can actually vary each year depending on your pay date and frequency.

- You have 4 options when it comes to dealing with an extra pay period. Depending on your decision, an extra pay period can also affect deductions, special wage payments, and income tax withholdings.

- Our checklist will help you keep track of everything affected by an extra pay period, whether it’s a leap year or not.

Leap years add an extra day of pay to the year. This increases the chance of an extra pay period, bumping the number from 26 to 27 for salaried employees paid biweekly (or from 52 to 53 for salaried employees paid weekly).

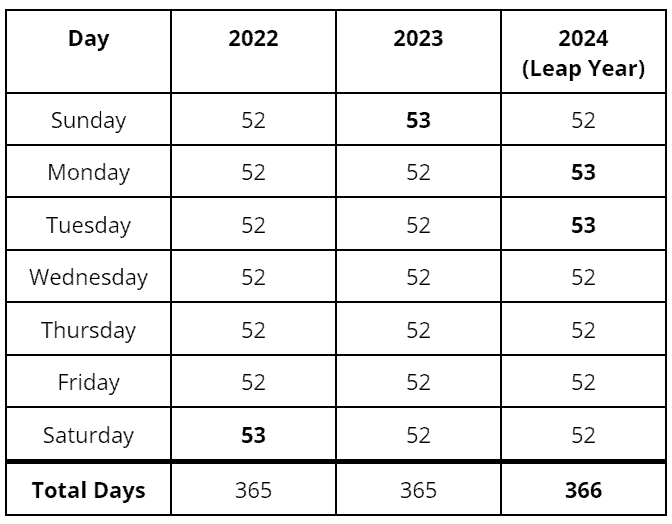

While leap years increase the probability of an extra pay period, the number of pay periods you have could actually fluctuate every year depending on your pay date and frequency. In any year that isn’t a leap year, there’s still one day of the week that occurs 53 times, instead of the normal 52. If your pay date falls on this day, you’ll have an additional pay period.

Because of this, you should count the number of pay periods you’ll have each year, regardless of whether it’s a leap year or not. If you have an extra pay period, you may need to adjust employee paychecks and deductions. See our table below for the number of days in 2022, 2023, and 2024 to help you plan accordingly.

Who is affected by an extra pay period?

An extra pay period can affect salaried employees paid weekly or biweekly. In 2024, there are 53 Mondays and 53 Tuesdays. As a result, weekly or biweekly salaried employees paid on either of these days will experience an extra pay period.

Salaried employees paid monthly or semi-monthly and employees paid by the hour are not affected.

How do you manage an extra pay period in payroll?

If you find yourself with an extra pay period, you have a few options for your payroll:

Option 1: Don’t make any changes.

Give employees their usual paycheck amounts each period. They’ll receive slightly higher salaries than normal at the end of the year. 86% of employers choose this option, despite the added cost it brings to their organizations. If you choose this option, inform your employees that their “raise” is due to the extra pay period and salaries will return to normal the following year.

Example: Mary is a salaried employee paid biweekly. In a regular year, she receives 26 paychecks of $1,538.46 each, totalling $40,000. In a year with an extra pay period, she receives 27 paychecks of $1,538.36, giving her a total salary of $41,538.46 at the end of the year, slightly higher than normal.

Option 2: Divide salaries by 27 or 53 (instead of the usual 26 or 52) to account for the extra pay period.

Choosing this option may put a strain on your employees. Even though their annual salaries will remain the same as years with 26 or 52 pay periods, they’ll receive smaller individual paychecks, which can affect their ability to cover bills and other regular expenses.

Example: Mary normally receives 26 paychecks of $1,538.46 each, but during a year with an extra pay period, she receives 27 paychecks of $1,481.48 each. Each paycheck decreases by $56.98, but her salary remains the same at $40,000.

Option 3: Divide salaries by a more accurate multiplier, either 26.0893 for biweekly employees or 52.1786 for weekly employees.

Salaries will fluctuate slightly year to year, but you won’t have to change your calculations from 26 to 27 (or from 52 to 53) each year depending on the number of pay periods. Instead, you can use 26.0893 or 52.1786 each year, no matter the number of pay periods.

Example: Whenever there are 26 pay periods, Mary receives 26 paychecks of $1,533.20 each. This adds up to a total salary of $39,863.09, slightly lower than her base salary of $40,000. In years with 27 pay periods, she receives 27 paychecks of $1,533.20 each, resulting in a total salary of $41,396.40, slightly higher than her base.

Note: In years where the base salary isn’t met, you’ll still have to pay the difference. In Mary’s case, she falls short of her base salary by $136.91 whenever there are 26 pay periods. Her employer will need to add this amount to her final paycheck so that she reaches $40,000 by the end of the year.

Option 4: Change your pay frequency or pay date.

If you pay employees semi-monthly or monthly, instead of weekly or biweekly, you’ll have 24 or 12 pay periods. Employees will receive larger paychecks less frequently, but their total salary will remain unchanged, and you won’t have to deal with an extra pay period.

Example: If Mary’s pay frequency is changed to semi-monthly, she will receive her $40,000 annual salary in 24 paychecks of $1666.67 each.

Alternately, consider changing your organization’s pay date to avoid extra pay periods. In 2024, for instance, there are 53 Mondays, but only 52 Fridays. If your pay date is Monday, you’ll have an extra pay period, but if you change your pay date to Friday, you won’t have an extra pay period.

No matter which option you choose, clearly explain to employees what changes you’re making to their paychecks (and why). While you may be tempted to choose the most cost-effective option (and there’s nothing wrong with that!), you should also consider how your decision will affect your employees. Smaller paychecks and disruptions to established pay schedules could lower your organization’s morale.

What else does an extra pay period affect?

Whether you continue payments as usual or make a change, an extra pay period can affect other factors connected to your payroll. To ensure your deductions and special wage payments are accurate for your number of pay periods, double-check these items and how you calculate them each year:

Health plan deductions

In most cases, your employees’ benefit deductions are calculated based on 26 or 52 pay periods. In years with 27 or 53 pay periods, these deductions will have to be recalculated or blocked in the additional pay period. For example, if your employees’ benefit contributions are scheduled biweekly, you could over-deduct if you don’t block deductions during the extra pay period. However, if your employees’ benefit deductions are taken twice per month, you won’t need to make any changes for an additional pay period.

Special wage payments

Some special wage payments are also based on 26 or 52 pay periods and will need to be recalculated in years with an additional pay period. One example is child support payments that are funded directly from employee wages.

Income tax withholding

The IRS doesn’t require changes to income tax withholding when there are extra pay periods, but you should still ensure calculations are adjusted appropriately. If you don’t, you might not withhold enough Federal income tax. Be sure to check state and local income taxes too, as the potential for under-withholding may be greater. Also let your employees know that they should adjust their calculations for income tax withholding if they want to withhold more or less than the standard amount.

Benefit contributions

The extra pay period can also affect how much your employees contribute to their 401(k)s, Health Savings Accounts (HSA), and Flexible Savings Accounts (FSA). If employees like to contribute the maximum amounts, they may have to change how much they deduct from each paycheck to reach that number by the end of the year.

Salary specifics documented in offer letters, contracts, and collective bargaining agreements

Before you decide how to compensate employees in a year with an extra pay period, review offer letters and other documents regarding compensation. Collective bargaining agreements are especially specific about pay periods and wages, so check them carefully. If these documents only state an annual salary, you can choose any of the above options to reach that amount. However, if the documents state that employees will be paid in weekly or biweekly checks of equal amounts, you must comply and choose Option 1 above.

For leap years only: an extra day

Leap years add an extra day to the calendar year, not just an added pay period. If any of your calculations depend on the number of days in a year, make sure you update that number in your formulas from 365 to 366. If you use a payroll provider, make sure they’ve accounted for February 29th in their system.

How does our checklist help?

Extra pay periods are more prevalent during leap years, but they can occur any year depending on your pay date and frequency. If you have an extra pay period, consider how you want to compensate employees and remember to check the other factors that may accompany payroll changes.

Our Complete Payroll Checklist for Leap Years and Extra Pay Periods will help you keep track of everything. If you need additional assistance, SentricHR’s all-in-one HRIS makes it easy to manage payroll and all of your HR needs. With our certified payroll and tax experts by your side, you can rest assured your payroll will be accurate and compliant each time. Speak with one of our product experts today!